India’s artificial intelligence startup ecosystem is expanding at a pace rarely seen in the country’s technology sector. Founders are launching AI-native products across healthcare, SaaS, fintech, education, legal services, customer support, logistics, agriculture, and enterprise automation. Venture capital firms are racing to identify the next breakout company. Incubators, state governments, and large enterprises are increasingly positioning AI as the foundation of India’s next startup wave.

While AI is expected to unlock major economic opportunities globally, India’s current AI startup boom also carries the ingredients for a significant correction. By 2028, the country may witness not just a handful of large AI successes, but also a far larger number of shutdowns, acqui-hires, distressed pivots, and underfunded startups unable to survive intensifying competition and shrinking differentiation.

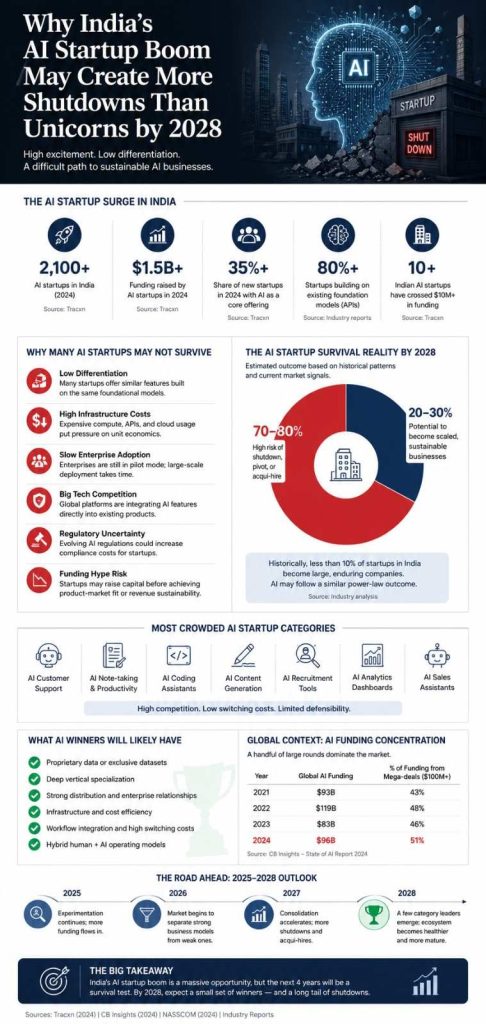

The pattern is not unique to India. Every major technology cycle — from dot-com startups to crypto platforms and quick-commerce ventures — has produced a long tail of failed companies beneath a small group of dominant winners. AI may follow a similar trajectory, but at a much faster pace.

India’s AI Startup Boom Is Real

India has rapidly emerged as one of the world’s largest startup ecosystems for applied AI innovation.

The momentum is being driven by several structural advantages:

- A large software engineering workforce

- Growing enterprise digitization

- Falling AI infrastructure costs

- Wider availability of foundation models

- Strong SaaS distribution experience

- Expanding cloud adoption

- Government-led digital public infrastructure

Indian startups are increasingly building AI products on top of large language models (LLMs), vertical AI agents, workflow automation tools, AI copilots, developer tools, healthcare diagnostics platforms, and multilingual AI applications tailored for Indian users.

Companies across sectors are experimenting aggressively with generative AI integration. Even traditional SaaS firms are repositioning themselves as AI-first businesses to remain competitive.

Investors have also responded quickly. Global venture firms, domestic funds, and corporate investors are allocating larger portions of capital toward AI-focused startups, particularly in enterprise software and productivity infrastructure.

Yet rapid startup creation does not necessarily translate into durable companies.

The Core Problem: Low Barriers to Entry

One of the defining characteristics of the current AI cycle is how easy it has become to launch an AI product.

A small team can now build a functional AI application in weeks using existing APIs and open-source models. Cloud infrastructure providers and AI platforms have dramatically reduced development complexity.

This democratization is positive for innovation, but it also creates saturation.

In many categories, startups are building nearly identical products:

- AI note-taking tools

- AI customer support bots

- AI sales assistants

- AI coding copilots

- AI content generation platforms

- AI recruitment tools

- AI analytics dashboards

The challenge is that many of these products are not defensible.

If a startup relies heavily on third-party foundation models without proprietary infrastructure, exclusive datasets, distribution advantages, or deep workflow integration, competitors can replicate features quickly.

This creates a dangerous market dynamic:

hundreds of startups chasing the same enterprise customers with limited differentiation.

The “Wrapper Startup” Risk

A growing concern among investors is the rise of what the industry informally calls “AI wrapper startups.”

These companies typically build thin application layers on top of existing AI models from providers such as OpenAI, Anthropic, or Google.

While some wrappers evolve into meaningful businesses, many struggle to maintain long-term advantages because:

- Core technology is externally controlled

- Margins are vulnerable to API pricing changes

- Platform providers may launch competing features

- Switching costs for customers remain low

This issue is particularly relevant in India, where many startups are optimizing for speed-to-market rather than proprietary research or deep infrastructure development.

Several investors privately acknowledge that a large percentage of current AI startup pitches appear interchangeable.

That does not mean all application-layer companies will fail. Some may win through execution, distribution, domain specialization, or workflow integration. But the market may not sustain dozens of similar products in every category.

Funding Abundance May Be Masking Weak Business Fundamentals

The availability of AI capital has created another structural risk: startups raising money before validating sustainable demand.

During periods of technological hype, investors often prioritize growth narratives over operational discipline. The AI cycle has shown early signs of similar behavior globally.

In India, some startups are scaling teams, marketing spend, and valuations before achieving:

- Reliable revenue retention

- Product-market fit

- Strong enterprise adoption

- Long-term monetization clarity

- Infrastructure efficiency

This becomes problematic because AI businesses can carry high operational costs.

Inference expenses, GPU access, cloud infrastructure, model fine-tuning, and enterprise deployment complexity can significantly impact margins. Companies offering low-cost AI services may discover that usage growth increases costs faster than revenue.

Unlike traditional SaaS businesses — which often benefit from strong software margins — AI-native businesses may face tighter economics if infrastructure dependence remains high.

The Global AI Consolidation Trend Could Hurt Indian Startups

Another major threat is platform consolidation.

Large global technology companies are moving aggressively into AI:

- Microsoft

- Amazon

- Meta

- Salesforce

- Adobe

These firms already possess:

- distribution scale

- cloud infrastructure

- enterprise relationships

- compute access

- proprietary datasets

- engineering depth

As AI features become embedded directly into existing enterprise software suites, standalone startups may struggle to compete.

For example, if productivity tools, CRMs, coding assistants, customer service software, and analytics platforms all integrate native AI functionality, smaller startups offering single-feature AI tools could face rapid commoditization.

This dynamic has already emerged in several Western markets, where some AI startups saw initial traction evaporate after platform providers launched similar capabilities.

Indian startups operating in highly horizontal categories may be particularly vulnerable.

India Still Faces a Deep Talent and Infrastructure Gap

Despite its engineering scale, India remains behind the US and China in frontier AI research infrastructure.

The country still faces limitations in:

- advanced GPU availability

- large-scale compute access

- foundational model development

- deep AI research talent

- semiconductor ecosystems

Most Indian startups are not building frontier models from scratch. Instead, they are focused on applied AI and enterprise implementation.

That is not inherently negative. Applied AI can generate significant value. However, it also means Indian startups often depend on external ecosystems controlled by global technology companies.

This dependency increases strategic risk.

If access costs rise, regulations tighten, or model providers alter commercial terms, smaller startups could experience margin pressure and operational instability.

Enterprise Adoption Is Slower Than Startup Expectations

Many founders assume AI adoption will happen rapidly across Indian enterprises. The reality is more complicated.

Large businesses continue to face concerns around:

- data privacy

- hallucination risks

- compliance

- integration complexity

- cybersecurity

- ROI measurement

Enterprise AI adoption cycles are often slower than founders anticipate.

Several companies are still in experimentation mode rather than large-scale deployment. Pilot programs do not always convert into meaningful contracts.

This creates a mismatch between startup growth expectations and actual enterprise buying behavior.

Some AI startups may run out of capital before adoption catches up.

The Market May Produce a “Power Law” Outcome

The likely outcome by 2028 is not the collapse of India’s AI ecosystem, but extreme concentration.

A relatively small number of startups may capture disproportionate value, while a much larger number struggle to survive.

The winners are likely to possess at least one of the following:

Proprietary Data Advantages

Startups with exclusive datasets or workflow intelligence may build stronger defensibility.

Deep Vertical Specialization

AI products tailored for sectors such as healthcare, manufacturing, finance, legal tech, or logistics may outperform generic horizontal tools.

Distribution Strength

Companies with strong enterprise relationships or existing SaaS customer bases could scale faster than new entrants.

Infrastructure Efficiency

Startups capable of managing inference and compute costs effectively may achieve healthier margins.

Hybrid Human + AI Models

Pure automation may not work in every sector. Businesses combining AI with human expertise may generate better outcomes and trust.

Not Every Shutdown Is a Failure

A high startup mortality rate is not necessarily evidence that AI itself is overhyped.

Technology cycles naturally produce experimentation, duplication, and consolidation.

Many startups that fail commercially still contribute:

- talent

- technical knowledge

- product innovation

- market education

Some founders will pivot successfully. Others may be acquired for talent or technology.

The broader ecosystem may ultimately emerge stronger after consolidation.

India’s previous startup waves — including e-commerce, edtech, food delivery, and fintech — followed similar patterns. Intense competition eventually produced a smaller set of dominant players.

AI may simply compress that cycle into a shorter timeline.

The Regulatory Landscape Could Also Change

Another underappreciated factor is regulation.

Governments globally are increasingly evaluating AI governance frameworks related to:

- data usage

- copyright

- misinformation

- algorithmic accountability

- consumer protection

- deepfake regulation

India’s regulatory approach toward AI is still evolving. Future compliance requirements could increase operational costs for startups, particularly smaller firms with limited legal and infrastructure capacity.

Regulatory uncertainty tends to favor larger, well-capitalized companies.

The Bigger Opportunity May Be AI-Enabled Businesses, Not Pure AI Startups

One emerging trend is that traditional businesses integrating AI effectively may outperform standalone AI-native startups.

Established SaaS firms, IT services companies, enterprise software providers, and industry-specific platforms already possess:

- customers

- distribution

- trust

- operational infrastructure

For them, AI becomes an enhancement layer rather than the entire business model.

This could reshape venture outcomes in India.

Instead of producing hundreds of pure-play AI unicorns, the ecosystem may see existing companies quietly absorb most AI-driven value creation.

What Investors Are Watching Closely

By 2026–2028, investors are expected to scrutinize AI startups far more aggressively on fundamentals than narratives.

Key metrics likely to matter include:

- revenue retention

- gross margins

- infrastructure efficiency

- enterprise conversion rates

- defensibility

- customer dependency

- usage economics

- proprietary workflows

- regulatory resilience

The market is gradually shifting from “Does this startup use AI?” to “Does this startup create durable value?”

That distinction may determine survival.

Conclusion

India’s AI startup boom is both real and significant. The country has a strong chance to become a major global hub for applied AI innovation, enterprise automation, and AI-enabled services.

But the current wave also carries clear warning signs.

Easy startup creation, crowded categories, infrastructure dependence, weak differentiation, and premature funding enthusiasm may create an ecosystem where closures outnumber breakout successes over the next several years.

The likely story of India’s AI era will not be one of universal failure or unlimited prosperity. It will be one of sharp selection.

A handful of companies may emerge as category leaders with sustainable business models and global relevance. Many others may struggle to survive the economic realities hidden beneath the excitement of the AI gold rush.

By 2028, India’s AI ecosystem may look less like a startup explosion and more like a highly competitive filtration process.

And that may ultimately be a healthier outcome for the industry.

Last Updated on Wednesday, May 20, 2026 11:17 am by Startup Chronicle Team