India’s travel fintech sector is entering a new growth phase, and Bengaluru-based startup Scapia is positioning itself aggressively for the next leg of expansion.

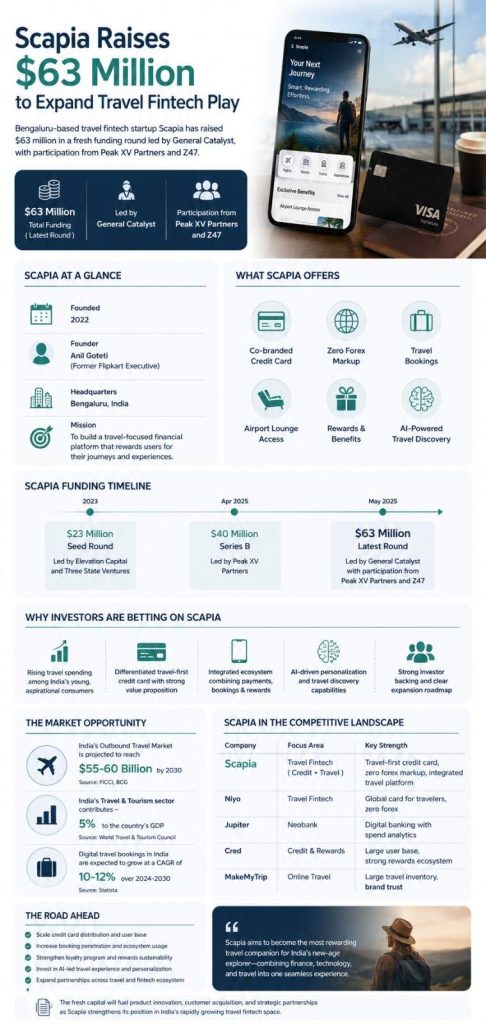

Scapia has raised $63 million in a fresh funding round led by General Catalyst, with participation from existing investors Peak XV Partners and Z47, according to reports published on May 21. The company plans to use the capital to scale its travel-focused financial products, deepen customer acquisition, and expand its integrated travel booking ecosystem.

The funding comes at a time when Indian fintech startups are increasingly shifting from broad consumer finance offerings toward category-specific ecosystems where payments, loyalty, commerce, and engagement intersect. Travel — particularly among younger urban consumers — has emerged as one of the most promising categories in that transition.

For Scapia, the latest raise is not just about adding capital. It is a test of whether a travel-first financial services model can build meaningful scale in a highly competitive Indian fintech market.

The Rise of Travel-Focused Fintech in India

Founded by former Flipkart executive Anil Goteti, Scapia launched with a relatively differentiated proposition: a credit card and travel platform designed primarily for frequent travelers rather than generic rewards users.

Its co-branded card partnership with Federal Bank helped the startup enter a crowded card market with a clear positioning around zero forex markup, travel rewards, airport privileges, and integrated bookings.

Unlike many traditional rewards cards that rely heavily on airline miles or bank-linked loyalty systems, Scapia has attempted to build a vertically integrated travel ecosystem where payments, bookings, rewards, and discovery remain inside the same app experience.

That positioning matters because India’s travel consumption patterns are changing rapidly.

According to multiple industry studies published over the past two years, younger Indian consumers are traveling more frequently, taking shorter trips, and increasingly booking through mobile-first platforms. Domestic tourism, cross-border leisure travel, and experiential spending have all rebounded sharply following the pandemic recovery cycle.

Scapia has attempted to capitalize on this behavioral shift by building financial products around travel frequency rather than purely around credit utilization.

Why Investors Are Interested

The fresh funding round reflects broader investor appetite for embedded finance and category-led fintech models.

Generalist fintech products have become harder to differentiate in India. Payments infrastructure has largely commoditized. Neo-banking models face monetization challenges. Consumer lending remains tightly regulated. In that environment, startups with strong engagement loops tied to specific lifestyles — travel, gaming, creator commerce, health, or education — are attracting renewed interest.

Scapia sits at the intersection of several large consumer trends:

- travel spending growth

- premium consumer finance

- rewards-driven engagement

- embedded commerce

- AI-assisted travel discovery

- cross-border payments

The company had previously raised $23 million in 2023 from investors including Elevation Capital and Binny Bansal’s Three State Ventures.

In April 2025, it raised another $40 million in a Series B round led by Peak XV Partners.

The latest $63 million raise significantly strengthens its balance sheet at a time when fintech fundraising remains selective despite improving venture sentiment.

Importantly, the round also indicates that investors are still willing to back consumer fintech companies if they demonstrate strong retention and ecosystem engagement rather than pure growth-at-all-costs metrics.

Beyond Credit Cards: Building a Travel Operating System

Scapia’s evolution over the past 18 months shows a deliberate effort to move beyond being “just another co-branded card.”

The startup has steadily expanded into adjacent travel services including:

- visa services

- train bookings

- bus bookings

- curated experiences

- AI-powered travel discovery

- travel commerce

- UPI-linked rewards products

Its newsroom announcements over the past year indicate a broader ambition to become a full-stack travel engagement platform rather than a narrow fintech app.

One of the more notable developments has been the launch of AI-driven travel experiences and curated discovery features. While many travel apps now claim AI capabilities, Scapia appears to be using personalization primarily to increase in-app engagement and transaction frequency.

That is strategically important because travel fintech economics are difficult if revenue depends solely on interchange fees or lending spreads. Companies in this category typically need multiple monetization layers:

- card interchange

- merchant commissions

- booking margins

- forex income

- partner revenue

- premium experiences

- loyalty ecosystem economics

The more time users spend inside the ecosystem, the more viable the model becomes.

A Crowded Competitive Landscape

Despite investor optimism, Scapia operates in an increasingly competitive segment.

The broader travel-fintech and premium consumer finance market includes players such as:

- Jupiter

- Niyo

- Uni Cards

- OneCard

- Cred

Traditional banks are also aggressively upgrading rewards ecosystems and premium travel offerings for affluent urban users.

In parallel, large travel platforms including MakeMyTrip and Ixigo are integrating fintech and loyalty products more deeply into their own ecosystems.

That creates a structural challenge for standalone travel fintech startups: retaining long-term differentiation.

The sector has already seen signs of pressure around rewards sustainability. Community discussions on Reddit and credit card forums indicate that some Scapia users have expressed concerns around reward devaluations and changing lounge-access thresholds earlier this year.

While such changes are common across credit-card ecosystems, they highlight a broader issue facing travel fintechs globally: balancing customer acquisition incentives with sustainable unit economics.

The Economics Problem in Travel Fintech

Travel fintech companies often face a difficult balancing act.

On one side, customers expect:

- generous rewards

- zero forex markup

- premium benefits

- travel discounts

- frictionless bookings

On the other side, startups must manage:

- high customer acquisition costs

- credit risk

- reward liabilities

- travel-margin compression

- compliance costs

- fintech regulation

This tension has already affected several global fintech and neo-banking players over the past few years.

For Scapia, long-term sustainability may depend less on rapid card issuance and more on whether it can create durable travel engagement and repeat transaction behavior.

The company’s recent expansion into experiences, travel shopping, and AI-powered discovery suggests management understands that challenge.

Why Timing Matters

The timing of Scapia’s funding round is notable.

Indian startup funding has recovered selectively in 2026 after a prolonged correction cycle between 2022 and 2024. However, capital allocation remains disciplined compared to the peak funding era.

Investors are now prioritizing:

- monetization clarity

- retention metrics

- ecosystem stickiness

- revenue quality

- operational efficiency

Scapia appears to have benefited from two favorable macro trends:

1. India’s Premium Consumer Expansion

India’s upper-middle-income consumer base continues to grow, particularly in metropolitan markets where travel spending is rising rapidly.

This demographic is highly attractive to fintech firms because users typically:

- spend more digitally

- adopt credit products faster

- travel more frequently

- transact internationally

- engage with rewards ecosystems

2. Travel Recovery and Behavioral Shift

Travel demand has structurally recovered post-pandemic, but consumer behavior has changed.

Younger travelers increasingly prefer:

- shorter leisure trips

- flexible bookings

- digital-first experiences

- reward-linked spending

- integrated payment ecosystems

Scapia’s model is closely aligned with these patterns.

The Regulatory Environment Remains Important

India’s fintech sector remains heavily influenced by regulatory developments.

The Reserve Bank of India has tightened oversight around digital lending, co-branded cards, KYC systems, and fintech-bank partnerships over the past few years.

For travel fintech startups, regulatory durability matters as much as growth.

Scapia’s partnership-led approach with Federal Bank may provide greater structural stability than models that rely heavily on loosely integrated fintech layers.

Still, scaling responsibly while maintaining compliance will remain a major operational challenge as the company expands.

What Comes Next for Scapia

The company’s next phase will likely focus on four major areas:

Scaling Card Distribution

Co-branded travel cards remain central to user acquisition and ecosystem engagement.

Increasing Booking Penetration

The more users book inside Scapia’s ecosystem, the stronger its monetization profile becomes.

Building Loyalty Infrastructure

Long-term retention will depend on whether rewards remain compelling without becoming financially unsustainable.

AI-Led Personalization

Travel discovery and recommendation systems may become an increasingly important differentiator as AI reshapes online commerce.

The Larger Significance of the Deal

Scapia’s funding round reflects a broader evolution in Indian fintech.

The first generation of Indian fintech focused on infrastructure:

- payments

- UPI

- digital banking

- lending rails

The next phase is increasingly about vertical ecosystems built around consumer intent and lifestyle behavior.

Travel is one of the few categories where:

- payments are frequent

- engagement is emotional

- loyalty matters deeply

- cross-selling opportunities are significant

That combination explains why investors continue backing the sector despite broader fintech caution.

Whether Scapia can convert strong investor confidence into a durable, scalable business will depend on execution over the next several years — particularly its ability to maintain customer engagement while protecting unit economics in a highly competitive market.

For now, the company has secured something increasingly difficult in India’s startup ecosystem: large growth capital tied to a clear category thesis.

Also Read : The Coming Collapse of Copycat AI Startups in India

Add Startup Chronicle as a preferred source on Google- Click Here

Last Updated on Thursday, May 21, 2026 8:54 am by Startup Chronicle Team